Personal Loans in April 2026: Rates, Trends and What They Mean for Borrowers

The financial pulse of 2026 is beating fast on the personal‑loan front. With the average APR hovering around 12.27%, lenders are tightening their offers while borrowers chase lower rates to consolidate debt or fund a home improvement project. The latest Bankrate snapshot, released April 29, shows that even though the market’s overall cost of borrowing remains stable, there is a noticeable shift toward shorter terms and tighter credit criteria.

How Do Current Rates Stack Up?

The average personal‑loan rate for April 2026 sits at 12.27%, based on data from Bankrate’s Monitor survey of the ten largest banks across the country. That figure reflects a typical three‑year term, a $5,000 loan amount, and a borrower with a 700 FICO score. Source

While the average remains in the low‑teens, the lowest available rates have dipped to 6.20%—the same floor seen in early January 2026. This drop is partly due to Bankrate discontinuing two high‑interest lenders from its tracking list on February 25, which shaved the median down by roughly a quarter of a percentage point.

Below is a quick snapshot of the most recent monthly low‑rate data:

| Date | Median Lowest Rate | Lowest Available Rate |

|---|---|---|

| 4/29/26 | 7.99% | 6.20% |

| 3/04/26 | 8.38% | 6.20% |

| 2/04/26 | 8.74% | 6.49% |

| 1/07/26 | 8.74% | 6.49% |

| 12/03/25 | 8.74% | 6.24% |

The Role of Credit Score and Loan Term

When you look beyond the headline average, a borrower’s credit profile becomes the main determinant of the rate they’ll receive. Lenders routinely reward those with excellent credit (typically 740+ FICO) with rates that can fall well below the market median—sometimes as low as 6.20% for a three‑year term.

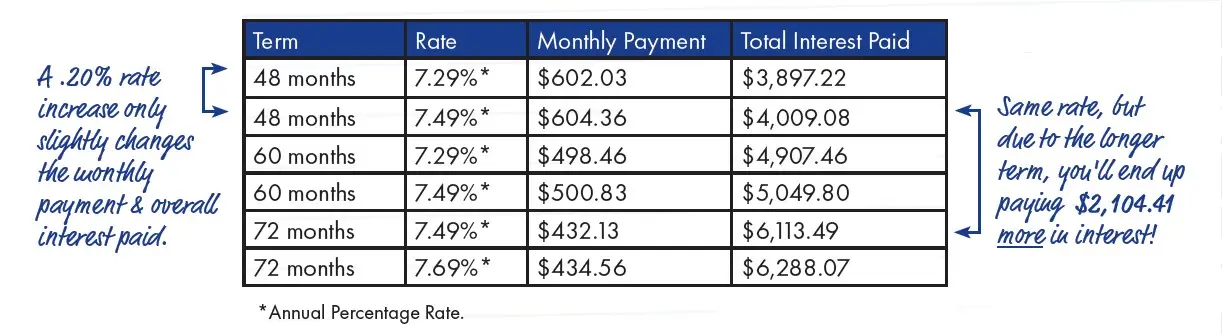

Conversely, borrowers with fair or sub‑prime scores may find themselves locked into the upper half of the spectrum, where APRs swing from 15% to even 30%. The Bankrate data shows that loan terms also influence rates: shorter terms (24–36 months) generally attract lower interest, whereas longer commitments (48–60 months) come with higher rates due to increased risk over time.

- Short‑term focus: A 30‑month loan for a $5,000 principal might cost you about 12% APR if your credit sits at 720.

- Longer horizon: Extending the same amount to 48 months could push that figure up to roughly 15%, assuming similar credit.

Online Lenders vs. Traditional Banks: Where Does the Money Come From?

The landscape is split between online fintech lenders and conventional banks or credit unions. Online platforms often advertise lower base rates, but they frequently tack on origination fees that can eat up 5–12% of the loan amount. In contrast, banks may offer more transparent pricing with no upfront fee, but their minimum balances and eligibility criteria are stricter.

Bankrate’s latest review highlights a few key players:

| Lender Type | APR Range | Typical Fees |

|---|---|---|

| Online Lenders (e.g., NerdWallet‑featured fintechs) | 6.25%–35.99% | Origination fee up to 12% |

| Commercial Banks (e.g., M&T Bank) | 6.99%–15.69% | No origination fee, but requires deposit account |

| Credit Unions | 6.09%–17.99% | Often no fees; membership required |

One practical tip: if you’re eyeing an online lender, ask whether the quoted APR includes any hidden charges. A low headline rate can be misleading if a hefty fee erodes your savings.

Why Lenders Are Tightening Their Criteria in 2026

The past year has seen a subtle shift toward stricter underwriting. With inflation still hovering above target and the Federal Reserve tightening monetary policy, lenders are more cautious about extending credit to riskier profiles. This is evident from the rising average loan-to-value ratios reported by Bankrate’s Monitor: borrowers now tend to borrow less relative to their credit score.

For example:

- A 700‑score borrower might receive a maximum of $7,500 in April 2026, down from $8,000 the previous year.

- In contrast, a 750+ score can secure up to $12,000 with similar terms.

This tightening is balanced by a corresponding decrease in default rates, which helps lenders maintain profitability while still offering competitive rates to high‑credit borrowers.

How to Spot the Best Deals Before You Apply

- Compare APRs, not just interest rates: The APR includes all fees and gives you a true picture of cost.

- Check for autopay discounts: Many lenders lower rates by 0.25%–0.50% if you set up automatic payments.

- Read the fine print on origination fees: A $500 loan with a 12% fee can cost an extra $60 in upfront charges.

Once you’ve gathered offers, plug them into a quick calculator to see how monthly payments stack up over time. Small differences in rate or term can translate into hundreds of dollars saved over the life of the loan.

Beyond the Numbers: What Borrowers Should Keep in Mind

While rates and terms are crucial, there are softer factors that often make the difference between a smooth borrowing experience and a stressful one:

- Customer service quality: A lender’s responsiveness can save you from late fees.

- Flexibility in payment schedules: Some lenders allow you to skip or pay extra without penalty.

- Reputation for transparency: Look for reviews that highlight how clear the lender is about hidden costs.

These qualitative aspects are often overlooked but can significantly affect your overall satisfaction with a loan.

Where to Find Up‑to‑Date Rate Comparisons

For the freshest snapshot of personal‑loan rates, Bankrate’s April 2026 rate page remains a go‑to resource. It aggregates data from over 10 banks and provides monthly updates on the lowest available rates, median APRs, and fee structures.

If you’re interested in exploring loan options quickly without a hard credit check, JetzLoan offers pre‑qualification tools that let you see potential rates based on your financial profile. The platform emphasizes transparent pricing and no hidden fees, making it a solid first stop for anyone looking to compare multiple lenders in one place.

Quick Rate Comparison Table (April 2026)

| Lender | APR | Loan Term | Origination Fee |

|---|---|---|---|

| M&T Bank | 7.99%–15.69% | 24–60 months | None |

| NerdWallet‑Featured Fintech (e.g., Upgrade) | 6.70%–35.99% | 12–84 months | Up to 12% |

| Credit Union Example | 6.09%–17.99% | 24–60 months | None |

When you’re ready to apply, remember that the APR is your best friend for comparing offers—especially when fees and payment flexibility come into play.

Final Thought: Timing Is Everything

The personal‑loan market in 2026 shows a clear trend toward tighter underwriting and slightly lower rates for top borrowers. For those with excellent credit, the window of opportunity to lock in rates near 6% remains open, but it closes quickly as lenders adjust their portfolios. Keep your credit score clean, shop around diligently, and consider using tools like JetzLoan’s pre‑qualification to stay ahead of the curve.